GEAR Token, Protocol and What Next

At Gearbox, we are building global lending rails for tokenised assets, designed to operate at scale and endure scrutiny. That mission comes with responsibility, and it also means confronting hard moments directly. A delisting from an exchange is not routine, and it is not something we dismiss or minimise. It is a serious development, and one we are addressing with transparency and intent.

This article provides a clear account of what led to the delisting, the choices we faced, and how protocol growth translates into long-term value for the GEAR token.

1. The Events, the Choices, and What Comes Next

A delisting by an exchange is not something we minimise or brush aside. It is disruptive, it reduces accessibility, and it can weigh on market sentiment. We understand the frustration this creates for investors and holders alike.

At the same time, it is important to clearly distinguish exchange listing mechanics from protocol fundamentals. This was a decision driven by market structure considerations, not an indication of any failure or degradation in the protocol itself.

1. a) What Led to the Delisting

GEAR is a DeFi-native token with a widely distributed supply. There is no centralized balance sheet, foundation wallet, or issuer that can be continuously deployed to manufacture liquidity on centralized exchanges.

In the current market environment, this matters more than it used to.

Across the industry, liquidity in long-tail assets has thinned materially. Remaining trading volumes are concentrated in a small set of large-cap tokens, while most altcoins face declining depth and inconsistent turnover. At the same time, exchanges have tightened listing standards, placing greater emphasis on sustained liquidity, order-book depth, and trading activity over time.

For tokens like GEAR, this creates a structural challenge. Without a constant influx of new external capital, maintaining exchange-level liquidity metrics becomes increasingly difficult, regardless of whether the underlying protocol continues to function, grow, or generate real usage. Over time, those dynamics compound.

The delisting was the result of these market-structure realities. It was driven by liquidity and depth thresholds, not by protocol health, security, solvency, or operational performance. The protocol continues to power credit across networks and protocols while positioning itself for the oncoming shift led by tokenisation.

I.b) The Choices we Had

This is not to suggest the protocol was without options. We had clear choices.

One option was to attempt to preserve the listing through aggressive intervention: deploying substantial treasury capital toward market-making programs, incentivising short-term volume, and optimising for exchange metrics rather than underlying fundamentals. This is a familiar playbook across the industry, particularly over the last cycle.

We chose not to take that path.

From the beginning, Gearbox has operated under a few non-negotiable principles. We do not centrally control token supply. We do not engage in artificial schemes or token pushes to manufacture activity. And we do not use treasury funds to create an appearance of liquidity that does not reflect real market demand.

There is also a pragmatic reason behind this decision. In the current environment, even heavy market-making spend increasingly fails to produce durable outcomes. Without new liquidity entering the market, these interventions tend to decay quickly, requiring ever-larger commitments just to maintain the same surface-level metrics.

At best, this delays the inevitable. At worst, it permanently weakens the protocol’s financial position without delivering long-term value.

We did not believe that expending meaningful treasury resources on short-term optics would serve the protocol, its users, or its long-term mission. Instead, we chose to preserve capital, remain aligned with our principles, and focus on building infrastructure that creates real, sustainable utility onchain. We explain what we believe is Gearbox's winning advantage in section 3 and 4.

I. c) Where the Fix lies

The uncomfortable truth about this phase of the market is that it rewards only two things.

First, hard financial engineering: aggressive liquidity provisioning, heavy incentives, and treasury-driven support that can sustain exchange metrics regardless of organic demand.

Second, real revenue-generating products with real users.

Gearbox has always been a product-first protocol. Usage has naturally expanded and contracted with market cycles, but the protocol itself has continued to function reliably throughout. Notably, the protocol has generated more revenue than it raised in July 2022.

That is why our view is straightforward. Sustainable product growth and genuine adoption are what ultimately change the revenue rut we have recently entered. And correct utilisation of this revenue is what creates durable liquidity, not the other way around. Over time, that is also what supports healthier market structure around the token.

For that reason, our budget, time, and focus remain directed where they have always been: shipping product, expanding real use cases, and building lending infrastructure that people actually want to use.

Section 3 describes what decides Gearbox's development further and what we are focusing on, the below section outlines how the protocol growth links back to the token growth.

2. Building around $GEAR

"Sustainable product growth and genuine adoption are what ultimately change revenue." is a line often followed by how does that growth translate into value for token holders, and rightfully so.

2.a) $GEAR buybacks

GEAR is not only a governance token. It captures value from protocol growth directly through buybacks.

Under GIP-219, 25 percent of realised monthly protocol revenue is allocated toward acquiring GEAR-WETH LP tokens on Uniswap V2. This increases liquidity depth, making GEAR more resilient to slippage, easier to enter and exit, and more attractive for external integrations, including CEXes.

At the same time, deeper liquidity improves the conditions under which the token trades. This mechanism represents the first phase of completing the protocol-to-token value loop in a compliant and strategic manner.

Future phases under discussion include increasing the share of revenue allocated to buybacks as revenue scales, expanding integrations that benefit the model, and evaluating additional mechanisms as regulatory clarity improves.

2.b) $GEAR alignment: No Equity Holders, Token Only

From the start in 2021, Gearbox Protocol has operated as a pure DAO, rooted in on-chain governance and community ownership. There’s no central foundation or corporate equity holder that can undermine the decisions of the DAO or claim it's revenue. Every dollar generated by the protocol feeds directly back into the DAO and the $GEAR ecosystem and there is only one asset for Gearbox Protocol: the GEAR token.

To conduct real-world operations: banking for vendors, contracts, payroll when needed and IP protection, the DAO engaged DAObox to establish a legal wrapper called Gearbox Foundation. This structure was first approved in late 2022, renewed after two years, and remains fully “ownerless” meaning it legally empowers the DAO without capturing equity or control.

This ensures compliance with closed‑loop DAO governance: the legal wrapper only acts as a conduit for DAO directives, never as a value extractor. Making GEAR token the sole beneficiary of protocol performance through buybacks.

2.c) 100% Circulation and Transparent Ownership

The GEAR token has been fully unlocked since July 2024, with no surprise unlocks or vesting cliffs remaining. The initial distribution went primarily to protocol users, early contributors, and strategic raises.

58% of GEAR supply went to the DAO while 42% was utilised for raises, early contributors and initial foundation. The Gearbox treasury still remains the largest GEAR holder with over 33% of the supply. While this supply remains 100% unlocked, it can not be issued without a prior governance proposal.

Further, Gearbox's raises were focused on participants who weren’t just passive holders; With participation from Cobie, Stani (AAVE), Variant, 1kx, Placeholder VC, Darren Lau and others, a large part of the GEAR supply went to notable voices who advised, supported, and governed the protocol when it was still finding its feet. Many of whom continue to hold and support.

You can find the complete list of participants, amount raised and more in the link below.

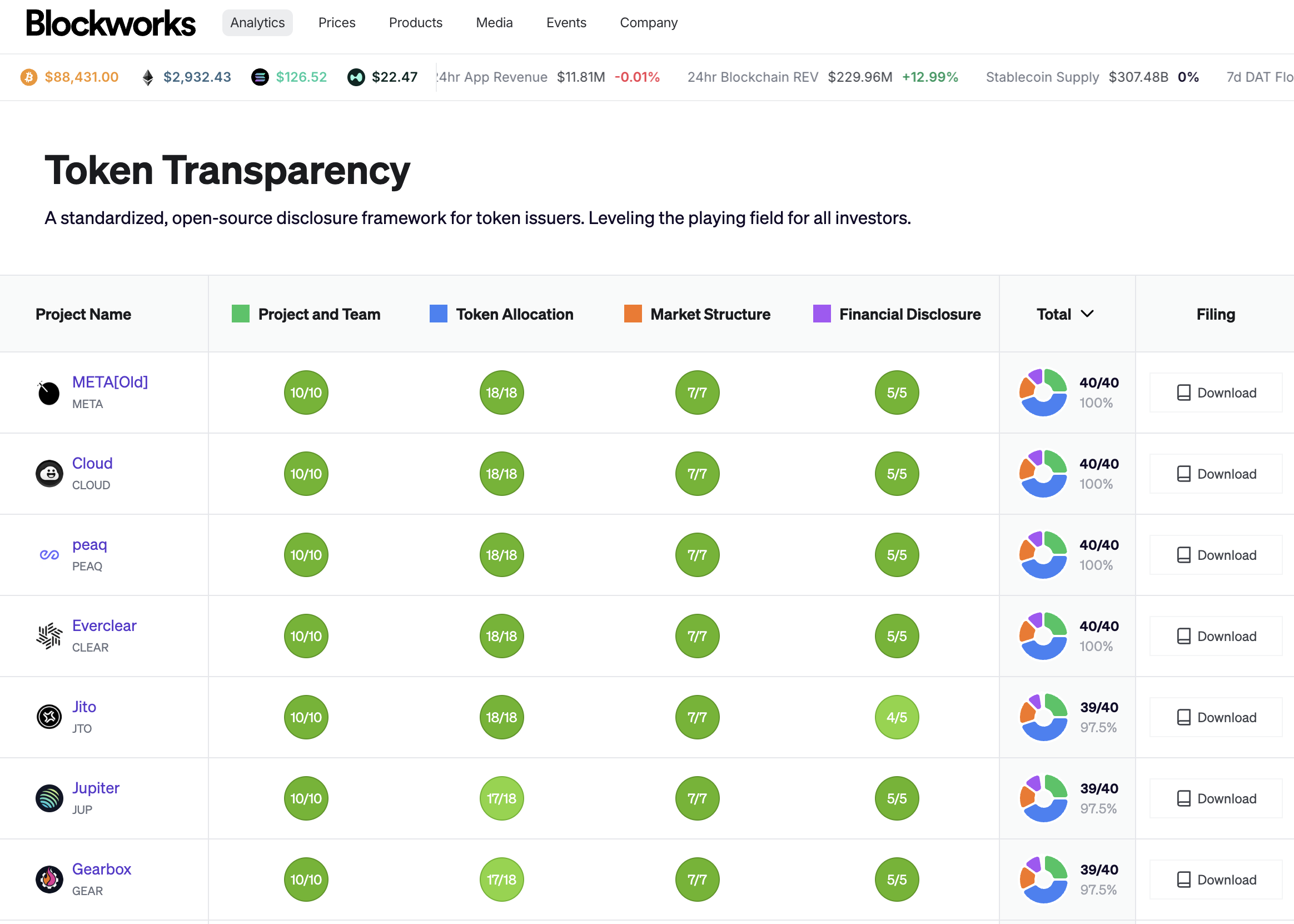

The GEAR token further boasts a score of 38.5 on Blockworks' Token Transparency Framework, making it one of the most transparent tokens in the industry.

These factors together ensure that the token isn't just a governance theatric but a transparent, value-capturing representation of the protocol's ownership and it's growth.

3. Where The Growth Comes From

Token value is one half of the equation. protocol growth is the other. To understand where the next leg of growth for lending protocols comes from, we need to understand the dominating trends currently shaping the industry.

3.a) Institutional Demand For Lending

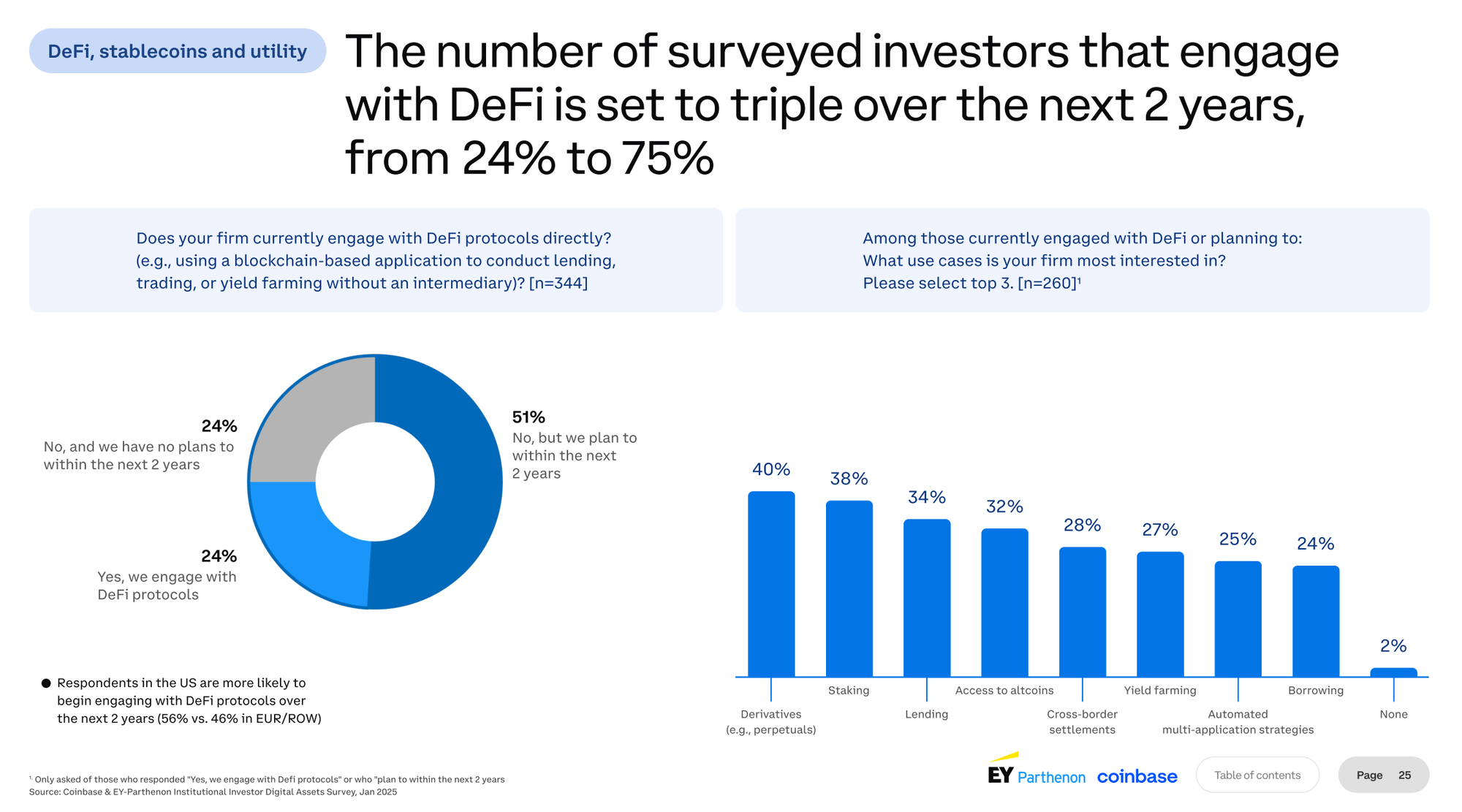

Institutions in DeFi aren't just allocating funds anymore, they are now active participants. With and through the likes of Superstate, Securitize, VanEck and more, institutions are now working to bring TradFi structures onchain. They either act as issuers of tokenised assets or allocators of capital. The current participation, though, is just the beginning. A recent report by EY and Coinbase surveying 300+ institutions suggests

• Number of key institutions onchain will more than 3X over the next 2 years

• 4 of the top 8 use cases relate to lending, borrowing, yield-farming and composable strategies.

With lowering retail participation, institutions are key for DeFi protocols to grow over the coming years. As a lending protocol, it is critical to position yourself to capture this oncoming growth.

Key to success: Replicating Institutional Grade Lending Onchain

3.b) Tokenisation of Everything

In the early days of DeFi, on-chain assets were limited to stablecoins, large-cap cryptos, and LSTs. But with regulatory headwinds softening and innovation accelerating, a whole new spectrum of assets is finding its way on-chain:

• RWAs

• Tokenized equities

• Tokenized basis yield

• Private credit

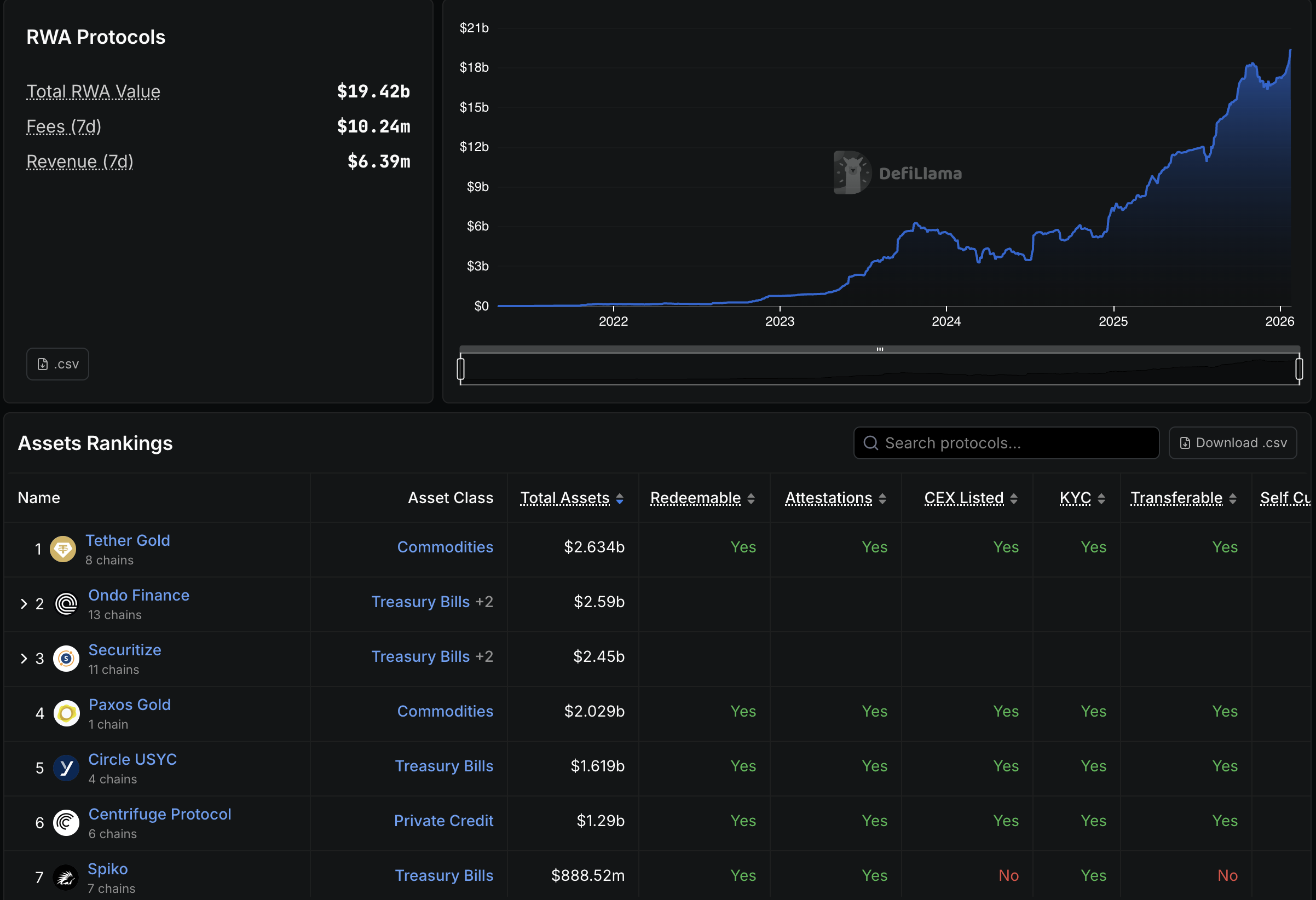

These new assets are now adding Billions of dollars and 1000s of users onchain every year, as seen by the growth of RWAs and Delta-Neutral yield products. Being early to these collaterals offers significant competitive advantage. For Lending Protocols to capture this growth, adding them in a safe, timely manner is key.

Key to success: Speed to Market and Ability for Tokenised Assets

3.c) Rise of the Curator Model

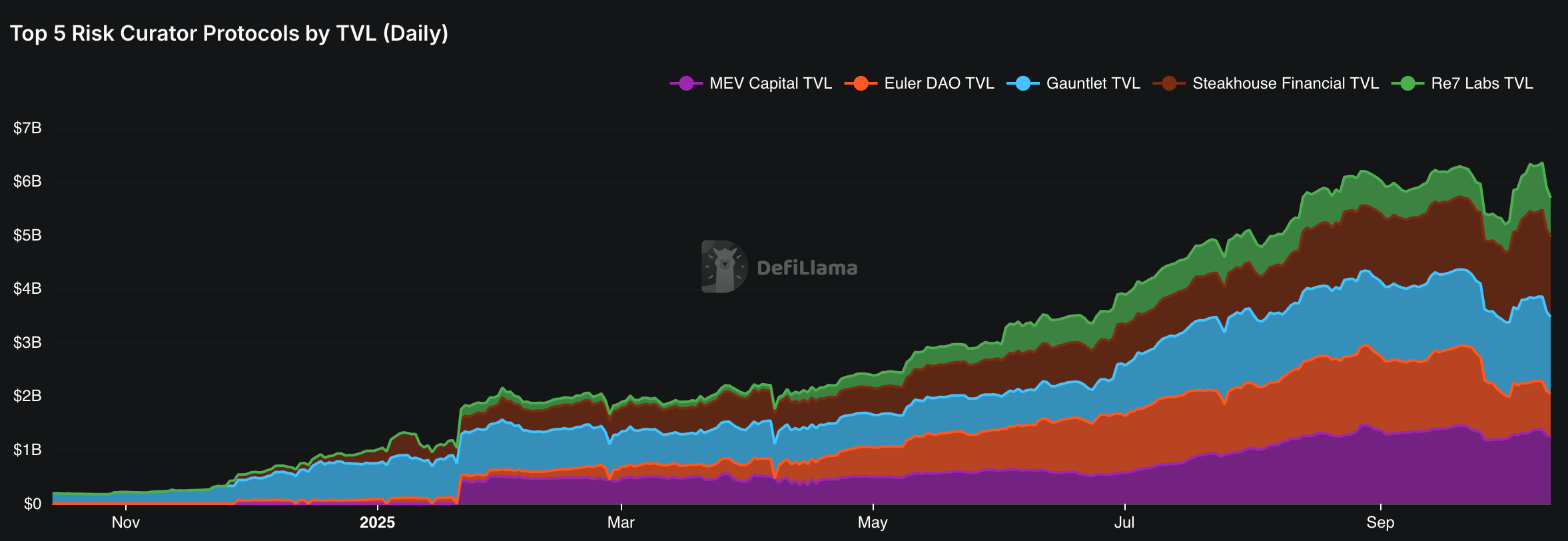

On one hand, institutions are driving the next wave of demand for on-chain lending, borrowing, and leverage. At the same time, relaxed regulations are unlocking new categories of collateral that once existed only off-chain. Bridging these two forces are Risk Curators, a segment that has grown over 2,000% in a year.

Risk curators design and manage specific risk parameters for various markets on lending protocols. They aren't developers but instead excel at risk management for specific assets. Instead of the DAO deciding what assets can be listed or how risk is priced, curators set their own collateral logic, oracles, and parameters to create markets they understand best. They earn fees based on the performance of their markets.

Key to Success: No code lending market creation by seasoned curators.

3.d) EVM led growth

The largest growing networks over the last 12 months have had 2 major things in common: They are purpose built and they utilise EVM.

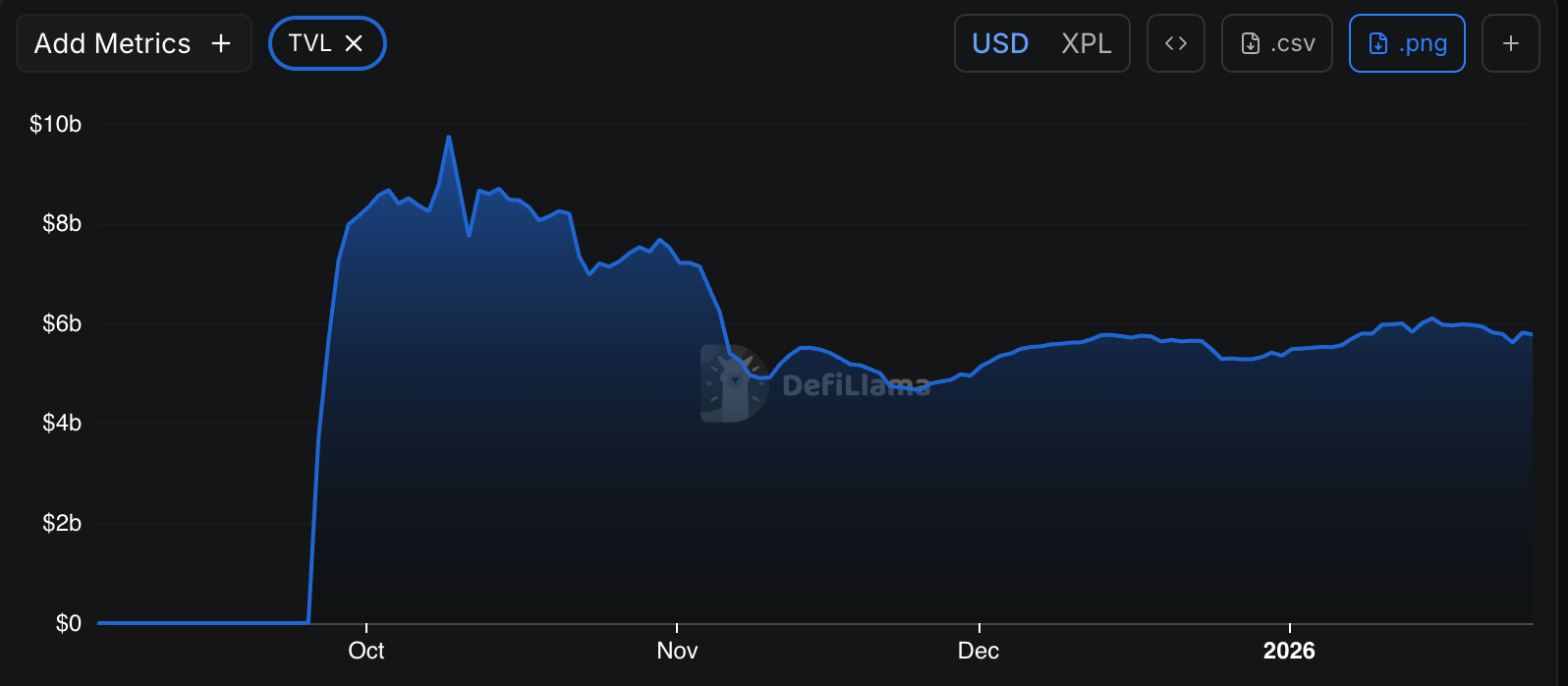

• Plasma: +$5.8B

• BSC: +$2B

• Base: +$2.4B

• HyperEVM: +$1.2B

Over the last 12 months, even without accounting for ETH mainnet, EVMs have gained over $10B+ in TVL, more than what the next 5 non-EVM networks gained during the same time. Given the network of applications and tools compatible with EVMs, this trend is likely to grow democratically.

Key for success: Simplified scaling across EVMs

3.e) Compliance Requirements

As institutions increasingly explore DeFi, assets issued and capital allocated by them increasingly looks for compliant markets. Regulatory clarity and institutional mandates now demand environments where compliance, transparency, and access controls coexist with decentralization. This is evident with the KYC requirement for projects like USDtb by Ethena, Tether Gold, Superstate, Centrifuge and other assets that have added $10B+ in TVL over the last year.

For protocols, this means evolving beyond purely permissionless architectures to include gated markets, isolated pools or permissioned layers that allow KYC’d institutions to lend, borrow, and deploy capital within defined regulatory frameworks. This dual design ensures that DeFi remains open at its core while still enabling regulated entities to participate, bridging the gap between institutional scale and decentralized innovation.

Key to success: Compliance tooling where needed

The trends that shape our industry today and keep growing sustainably all point towards a similar direction: institutional grade lending rails for tokenised assets.

4. Why Gearbox Captures Growth from Tokenised Assets

Tokenisation and RWAs have become the most credible growth vector for onchain protocols. Nearly every major protocol now claims an ambition to capture this growth.

The more relevant question, however, is not whether RWAs will drive the next phase of onchain activity, but which lending infrastructure is actually designed to support them. That distinction is where we believe Gearbox has a structural advantage.

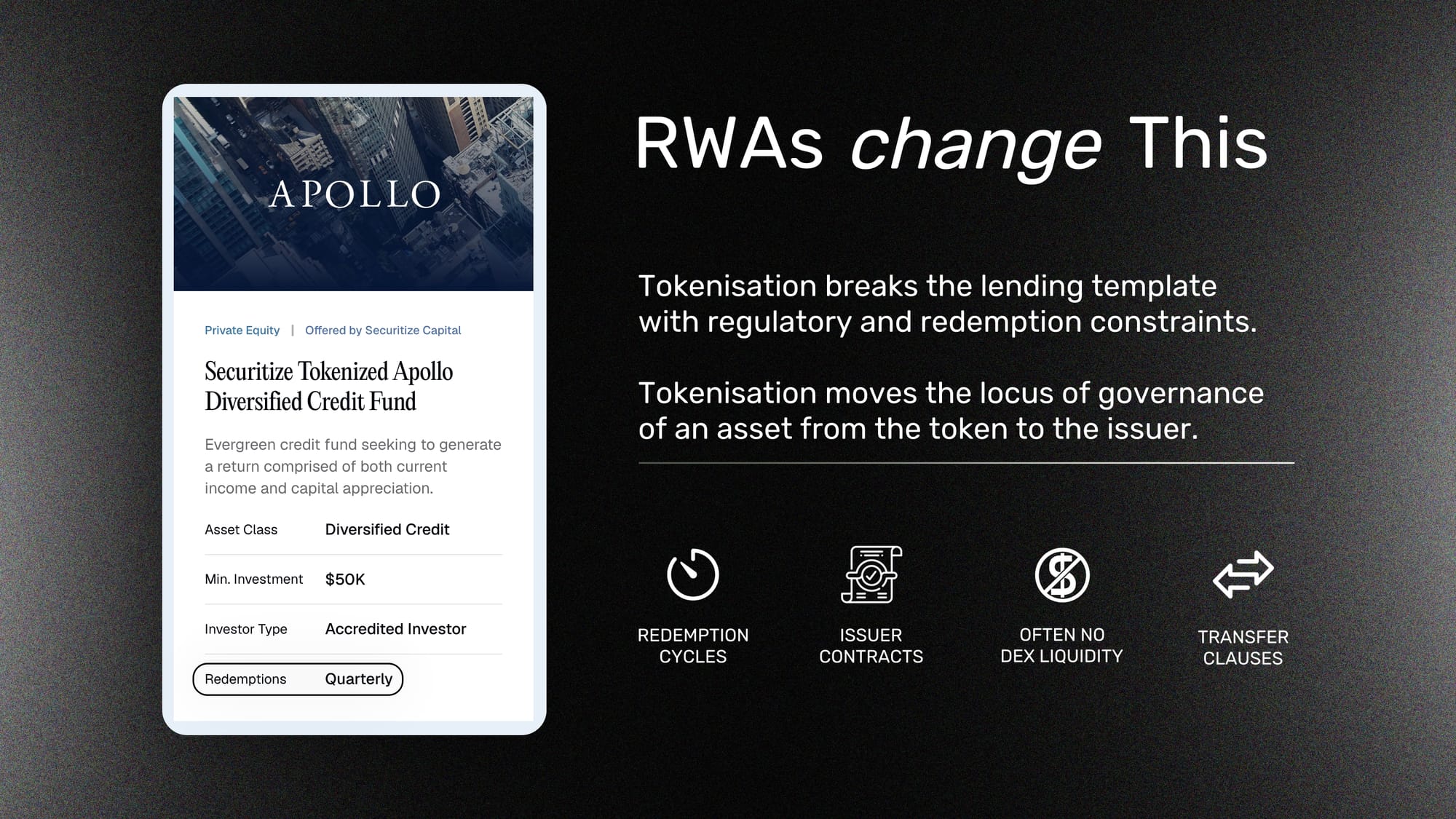

4.a) Tokenised Assets aren't Like Onchain Collaterals

Tokenising an asset does not just bring the asset onchain, it also brings along the legal, regulatory, and operational constraints that exist in the real world. These constraints shape how the asset behaves as collateral and on lending protocols.

Tokenised assets differ materially in how they operate day to day: how and when they can be redeemed, how often they are valued, and how quickly positions can be reduced. These mechanics directly affect subscription and redemption mechanisms, liquidation timelines, and compliance management. Two assets can both be classified as RWAs and still behave nothing alike once they are used as collateral.

Most importantly, liquidity for tokenised assets is not guaranteed. Regulatory rules, transfer restrictions, redemption gates, and issuer controls determine who can step in during stress and whether liquidity is available through secondary markets or only through the issuer. This is why DeFi lending models built for onchain-native assets do not automatically extend to tokenised ones. Tokenised assets are fundamentally different collateral, and they must be treated as such.

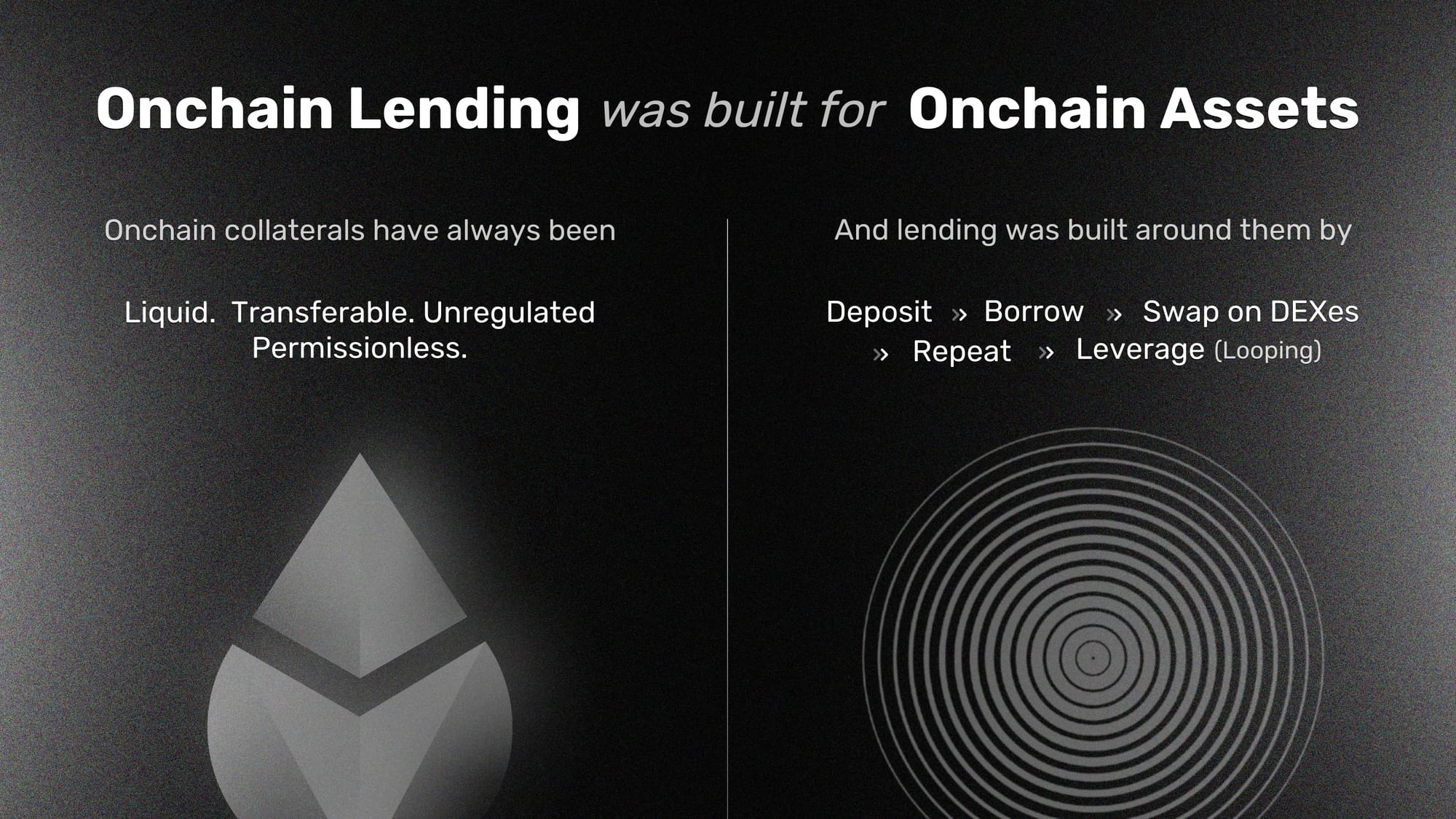

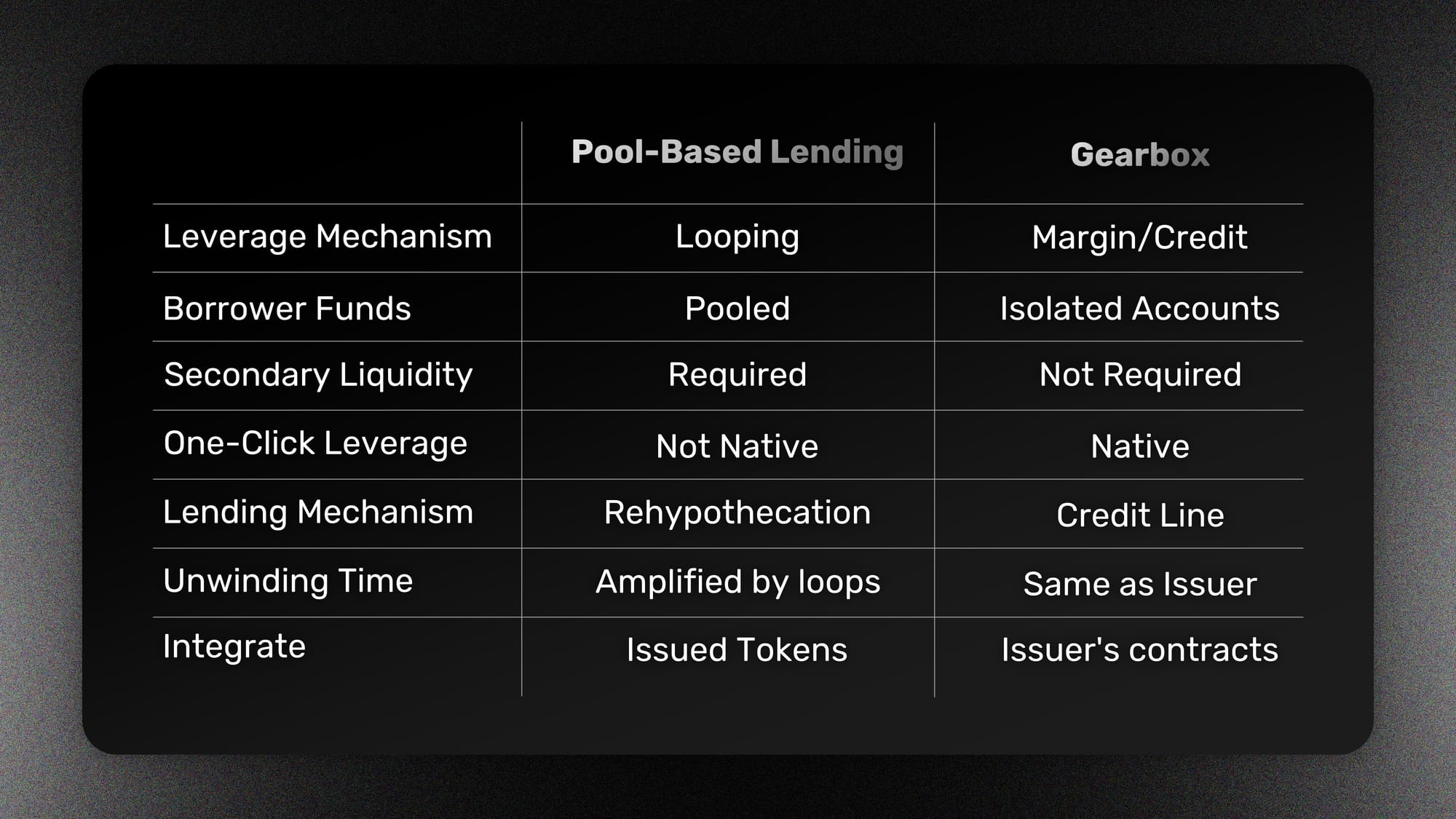

4.b) Onchain Lending was built for Onchain Collateral

Onchain collateral has historically followed a common template. Whether it was an LST, an LRT, or a yield-bearing stablecoin, these assets were liquid, freely transferable, and permissionless by design. They conformed to common token standards like ERC-20 or ERC-4626, making them easy to integrate across protocols. Crucially, they had deep secondary liquidity on DEXes, allowing positions to be exited through swaps rather than redemption. There were no issuer controls, jurisdictional restrictions, or regulatory gates. The token itself was the asset.

Pool lending protocols were built around this assumption. They integrated token standards rather than issuer logic, relied on DEX liquidity for liquidations, and enabled leverage through looping and flash loans inside a common pool. RWAs break this model. Tokenised assets do not follow a shared template and are not governed primarily by their token interface. They are constrained by issuer mandates, redemption cycles, transfer restrictions, and regulatory requirements, often with no secondary liquidity by design. Tokenisation brings assets onchain, but control remains with the issuer. As a result, RWAs are fundamentally incompatible with lending infrastructure designed for permissionless, onchain-native collateral.

4.c) Real World Assets need Real World Lending

Tokenisation does not create new assets, it brings real-world assets onchain. Lending against them does not require new financial primitives, only the replication of how credit works offchain. In traditional finance, assets are not financed through pooled rehypothecation or recursive borrowing. They are financed through margin accounts, credit lines, and structured lending vehicles like CLOs. Borrowers do not repeatedly deposit and borrow the same asset to reach leverage. They access credit, then use that capital to acquire the asset directly from the issuer.

Gearbox follows this same model onchain. Instead of looping assets through pools, users open isolated Credit Accounts that allow them to borrow multiples of their deposited collateral. Those borrowed funds can be used to subscribe directly to RWAs through issuer contracts, without relying on DEX liquidity, flash loans, or secondary markets. A leveraged RWA position is opened in a single transaction: collateral is deposited, credit is drawn, and the asset is minted at the source. This structure eliminates slippage, fee leakage, and unwinding delays, while enabling faster redemption and borrower-specific regulatory controls.

By offering credit at the account level and aligning with issuer workflows, Gearbox brings real-world credit mechanics onchain, making RWAs usable under leverage in the way they were designed to be financed.

This structural advantage means Gearbox does not need to overhaul its protocol or rush to accommodate each new class of collateral. Instead, it allows the protocol to offer battle-tested, enterprise-ready lending infrastructure that institutions can rely on.

Coupled with the GEAR token flywheel, this positions Gearbox to capture a category of growth that few protocols are structurally equipped for, while enabling token holders to directly benefit from that growth.

5. How the Protocol has Fared With the "Trends"

Gearbox's work on capturing this EVM, compliance and RWA led growth isn't a theoretical growth strategy but a key operational pivot already under way and growing.

5.a) DeFi's first RWA Credit-Line

Gearbox's RWA driven lending product isn't a work-in-progress concept but a core offering. During the Holidays, Gearbox went live with the first RWA credit line for Midas and has surpassed $30M in TVL.

Borrowers burn billions on slippage. Issuers lose millions bootstrapping liquidity. DeFi loses efficiency. No more.

— Gearbox Protocol (@GearboxProtocol) December 24, 2025

The first real credit-line for RWAs is now live. Mint mEdge via @MidasRWA's contracts with up to $1M in credit.

0 slippage, 0 DEX reliance, 7X faster unwinding↓ pic.twitter.com/HEHrX6mRJc

Users can access up to $1 million in credit while minting mEDGE through issuer contracts by Edge Capital. Why does this matter?

• The asset has no DEX liquidity

• No instant redemption: 2 day wait

• No flashoans: No looping available

And yet Gearbox unlocks lending and leverage without slippage, DEX liquidity costs or even redemption delays (where looping products would require 14 days to exit). Essentially, Gearbox delivers the same subscription and redemption mechanism but with borrowed capital and a larger size. Unlocking true enterprise-grade lending onchain.

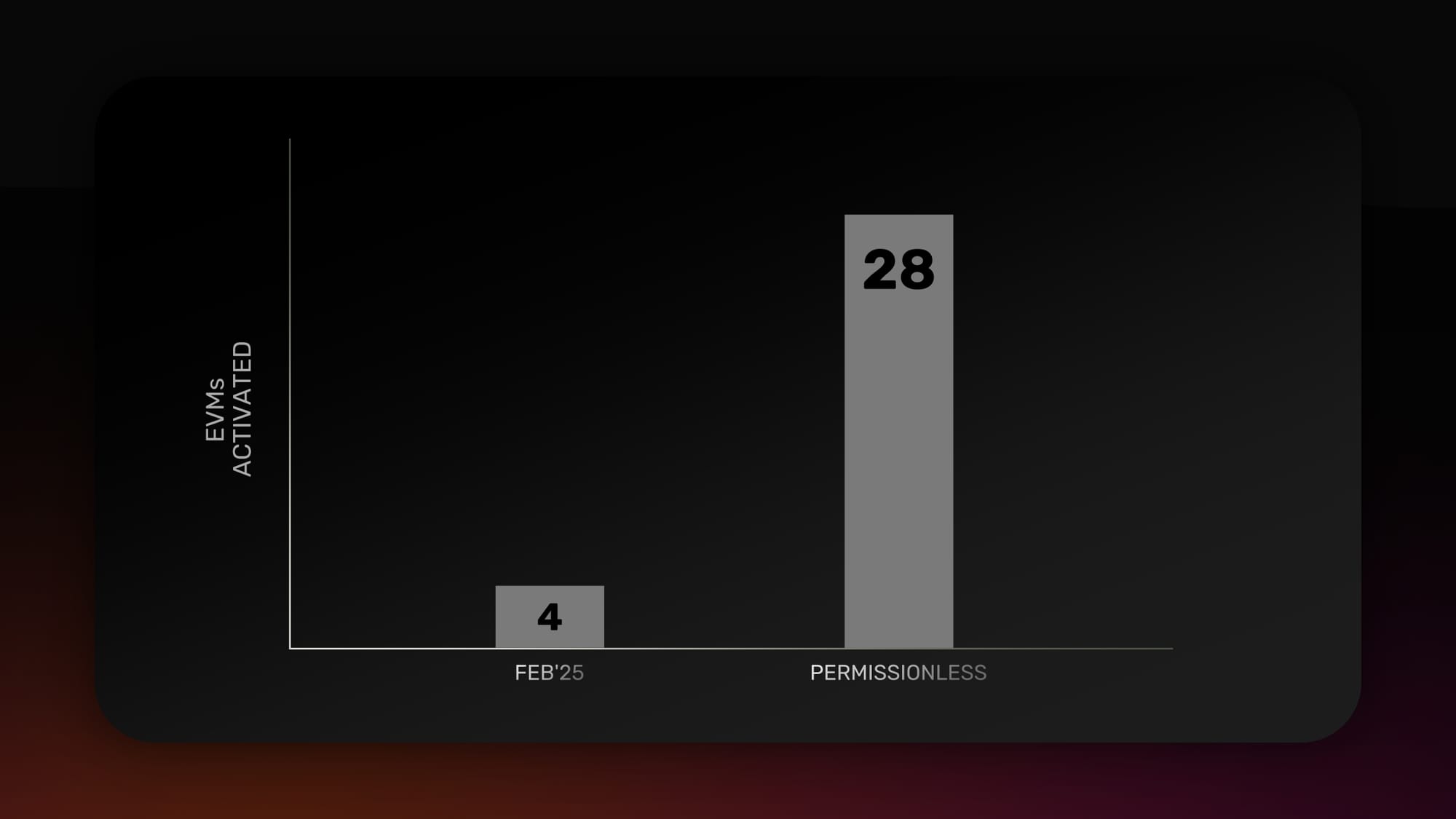

5. b) Reaching where RWAs are: Omni-EVM Architecture

RWAs have displayed a preference for purpose-built networks. To capture their growth, Gearbox thus needs to rapidly scale to said networks.

And over the last 6 months saw Gearbox has been activated on 28 EVMs, 7X more than we were on back in March'25. The ability to rapidly scale on L1 and L2 EVMs enables Permissionless to capture over $100s of Million in growth.

• Monad, curated by Edge: $50M+ peak TVL

• Plasma, Curated by Invariant Group: $80M+ peak TVL

• Etherlink, curated by Re7: $20M+ peak TVL

The RWA credit line instance by Gearbox and Midas has also been deployed on Monad, made possible by Gearbox's omni-EVM architecture. With more tokenised assets spreading across EVM networks, this aspect is crucial to capture the growth.

While Gearbox is activated on 28 EVMs, it's operational on 10. This enables DAO to significantly operational costs while still being available for market creation on numerous EVMs.

5.c) Curator Adoption

Gearbox during this period has been able to attract 8 new curators with a combined AUM of $3B+ across kpk, Edge, Tulipa, K3 and others. 4 of the curators working on Gearbox today are amongst the top 15 curators in DeFi, a clear sign of Institutional adoption.

Curators are key to understanding market risks and setting-up the no-code lending markets tokenised assets require. Adding institutional curators is key to future-proof growth.

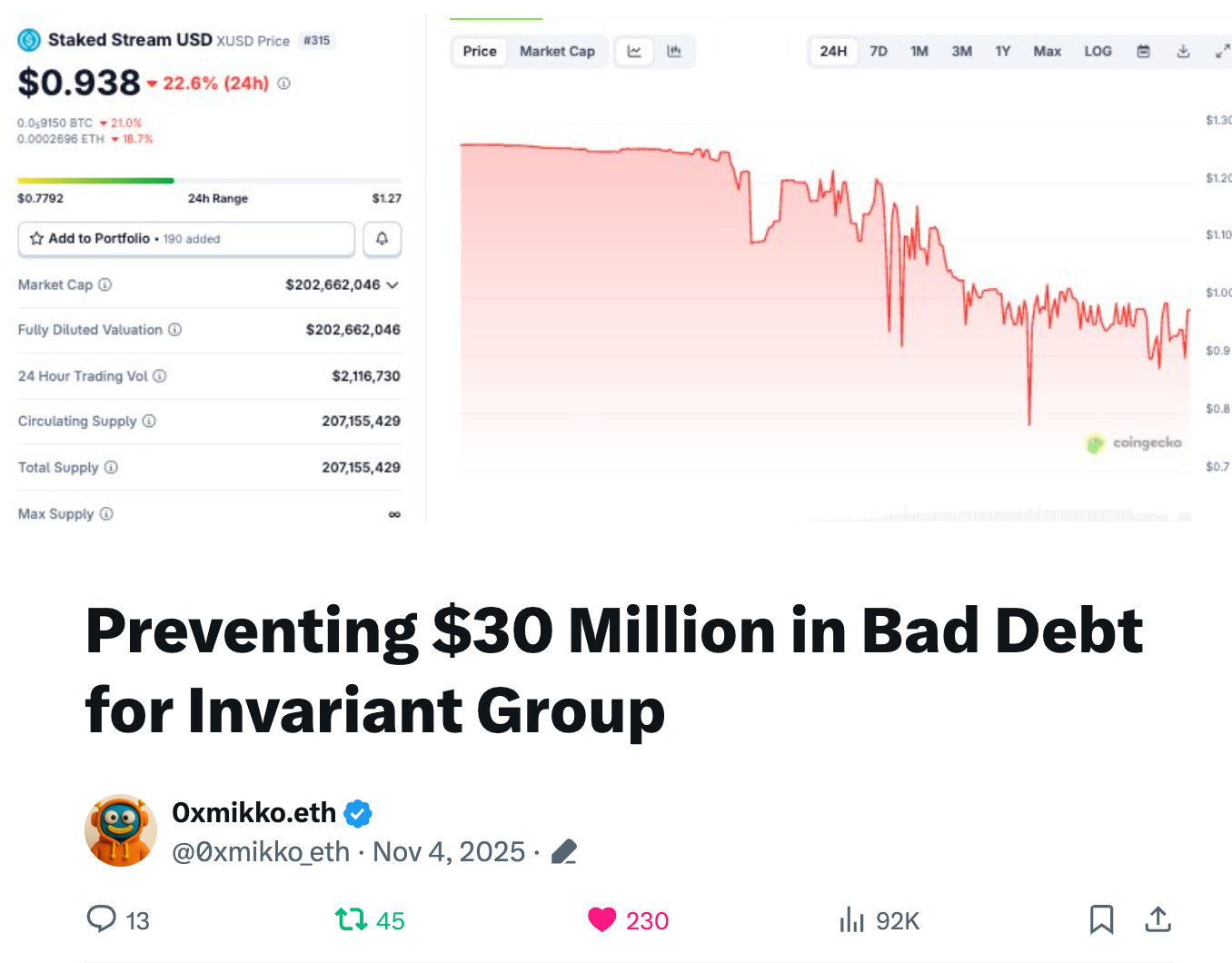

5.d) Battle-Testing: Faring Through xUSD Implosion

The collapse of StreamDeFi's xUSD was one of the most painful risk events to occur in DeFi since TerraLuna's UST. While users in anguish can never be a net positive for the space, it provided protocols a stress test for complicated assets and tested their designs.

Tokenised assets tend to have more complexity than the usual LRT or LST. A default in private credit directly leads to collateral quality evaporating, a loss in a tokenised yield strategy leads to the collateral losing value. The risks for these assets are incredibly dynamic and so is an institution's approach towards managing the said risks.

xUSD's collapse led to bad-debt on every major lending protocol apart from Gearbox despite $30M+ of exposure because Gearbox was built with this view. While other protocols forced curators to hardcode parameters, curators on Gearbox were able to adapt to changing risks to keep their lending markets safe. This battle testing was key to establish Gearbox's performance in comparison to our competitors and serves as a key example of how it works for institutions. You can read the complete details below.

5.e) Developing the RWA Product Line

For Gearbox to extend credit directly against RWA-native contracts, integrating the issuer's contracts remains key work. Unlike standard onchain collateral, issuer contracts embed asset-specific logic around minting, redemption, compliance, and control, all of which must be explicitly supported by the lending infrastructure. Gearbox has already done this work at scale, having built custom integrations for protocols such as

• Morpho

• Mellow

• Midas

• Upshift

Enabling credit to be deployed directly into their contracts rather than routed through generic pools. Products around these protocols can be sent live by curators soon.

In parallel, the protocol has held substantive conversations with some of the largest issuers in the space, including Securitize, around designing tokenised lending products that align with issuer requirements.

Beyond crypto-native integrations, Gearbox has also established relationships with traditional lending institutions, with $20B+ in AUM, and operators to co-develop products that can translate real-world credit demand into durable, onchain protocol growth. While much harder to convert, this approach correctly represents Gearbox intentions of not being a CT driven protocol.

Ending Note

We are aware a significant segment of the holders won't agree with the choice we had to make. We are aware a significant segment will find capturing growth via RWAs to be a task too hard to deliver. But a delisting is a moment to reassess priorities, not abandon them. For GEAR holders, it reinforces a core belief that has guided the protocol from the start: the token’s long-term value is driven by real economic activity and revenue.

With the onchain economy changing, that sustainable source is no longer onchain assets but the real assets that are being tokenised and brought onchain. Market liquidity will continue to move in cycles, and short-term narratives will always fluctuate. What remains constant is that tokens accrue durable value only when they represent ownership in systems that generate sustainable revenue and usage. As Gearbox expands into institutional lending, tokenised assets, and compliant credit markets, the GEAR token remains the sole vehicle through which protocol performance is reflected, via governance and direct value capture mechanisms.

GEAR is not designed to win on optics or temporary incentives. It is designed to represent ownership in a lending protocol built for the next phase of DeFi. As tokenisation accelerates and real-world assets become a structural part of onchain finance, we believe this alignment positions the GEAR token to benefit from growth that is measured not in optics or liquidity, but in durable adoption, revenue, and long-term value creation.

If you are an institution or curator looking to expand your operations onchain, Gearbox can offer you the RWA credit infrastructure you require. Contact us on Telegram or Discord, and get in touch. Let’s build the onchain economy together!

- Website: https://gearbox.fi/

- Main App: https://app.gearbox.fi/

- Telegram: https://t.me/GearboxProtocol

- Discord: https://discord.gg/gearbox

- Twitter: https://twitter.com/GearboxProtocol

- User Docs: https://docs.gearbox.finance/

- Developer Docs: https://dev.gearbox.fi/

- Github: https://github.com/Gearbox-protocol

- Snapshot page: https://snapshot.org/#/gearbox.eth