Reclaiming Composability: Why DeFi’s Most Important Advantage Remains Underused

Composability has long been positioned as DeFi’s strongest structural advantage. In principle, it enables financial systems to interact seamlessly, allowing users and institutions to assemble complex strategies by combining independent protocols. This capability should unlock efficiencies that traditional finance cannot replicate. Yet despite its prominence, composability in practice remains far more limited than its potential, particularly in lending.

Most lending integrations today are integrations in name rather than function. That is because lending protocols typically understand only the token standard, the ERC-20 representation, rather than the redemption rules, withdrawal flows, or settlement mechanics of the protocol issuing that token. As a result, the industry has built an ecosystem that appears interoperable on the surface, yet offers little of the true functionality that composability promises.

To understand why this gap persists, and why it must be addressed before RWAs and institutional capital can scale onchain, we must examine how current architectures constrain composability, what composability should actually mean, and what kind of infrastructure can support it.

The Difference Between Token-Level and Protocol-Level Composability

The industry often treats composability as a binary state: either a lending market “supports” an asset, or it doesn’t. But support is not composability. True composability preserves the functional behaviour of one protocol when accessed through another.

When a lending protocol lists stETH, for example, that does not make it composable with Lido. If a leveraged stETH position cannot be unwound through Lido’s actual withdrawal mechanism, the queue, validator exits, and settlement process then the interaction being offered is not with Lido the protocol, but with a token that only delivers you it's yield.

The same dynamic appears across major DeFi systems:

- Pendle PTs redeem principal at maturity without market friction. If a user with leverage must rely on AMM liquidity to redeem PTs, the core guarantee Pendle provides is lost.

- Mellow LRTs are designed for zero-fee minting and redemption. Yet on most lending markets, the only exit path for leveraged positions is through DEX pools that introduce cost, slippage, and liquidity risk.

- Convex positions generate meaningful economic value, but because they are not tokenised, pool-based lending systems cannot recognise or integrate them at all.

In each case, the token is supported, but the underlying protocol’s behaviour is not preserved. Composability becomes symbolic rather than structural.

This is not a matter of poor execution, but of architectural limitations.

Why Pool-Based Lending Models Cannot Deliver Real Composability

Traditional lending markets rely on a pool-based architecture: users deposit assets, the system aggregates them, and borrowers draw from a shared reserve. It is efficient for simple borrowing, but fundamentally mismatched with the kind of composability DeFi aspires to.

A useful analogy is the vending machine. A vending machine accepts an input and dispenses an output of value lower than the input, but it does not understand the context, the lifecycle, or the mechanics of the items it holds.

Pool-based lending works the same way. It can store tokens, price tokens, and liquidate tokens but it cannot participate in the functionality of the protocols those tokens come from.

Pools, utilising risk parameters, try to ensure:

- all collateral can be liquidated instantly on open markets

- all value is fully represented in token form

- the asset’s economic behaviour is constant over time

- redemption or settlement can be substituted with secondary liquidity

But many modern DeFi assets, and nearly all real-world assets, are defined precisely by the constraints that violate these assumptions. They have maturity terms, withdrawal queues, issuer-controlled redemption rules, or settlement windows that cannot be abstracted away.

When pool architectures encounter such assets, the only available fallback is to substitute protocol-native interactions with DEX trades, often forcing issuers to pay for DEX liquidity for token integrations. And at that moment, composability collapses.

What Composability Should Look Like

To restore DeFi’s original vision, composability must be defined more rigorously:

A protocol is composable with another when a user can interact with it through borrowed capital with the same functional efficiency as if they were interacting with it directly.

In existing DeFi protocols, this would look like:

- Lido: Leveraged stETH positions should be able to unwind through Lido’s actual withdrawal mechanism rather than synthetic alternatives.

- Pendle: Leveraged PT strategies should allow redemption at maturity exactly as Pendle allows, without DEX costs.

- Mellow LRTs: Users should be able to mint and redeem LRTs at zero fees, regardless of leverage size.

- Convex: Non-tokenised positions should still be credit-eligible through accounting that recognises their economic value.

This standard requires:

- respecting native redemption mechanisms (Pendle PTs, Lido withdrawals)

- preserving fee structures (zero-fee minting for Mellow LRTs)

- recognising economic value that is not tokenised (Convex positions)

- integrating the protocol’s contracts, not just its outputs

Under this definition, composability is not about listing more tokens; it is about enabling more capabilities.

And achieving this requires a fundamentally different infrastructure approach.

Credit Account Architecture: The Missing Foundation for Real Composability

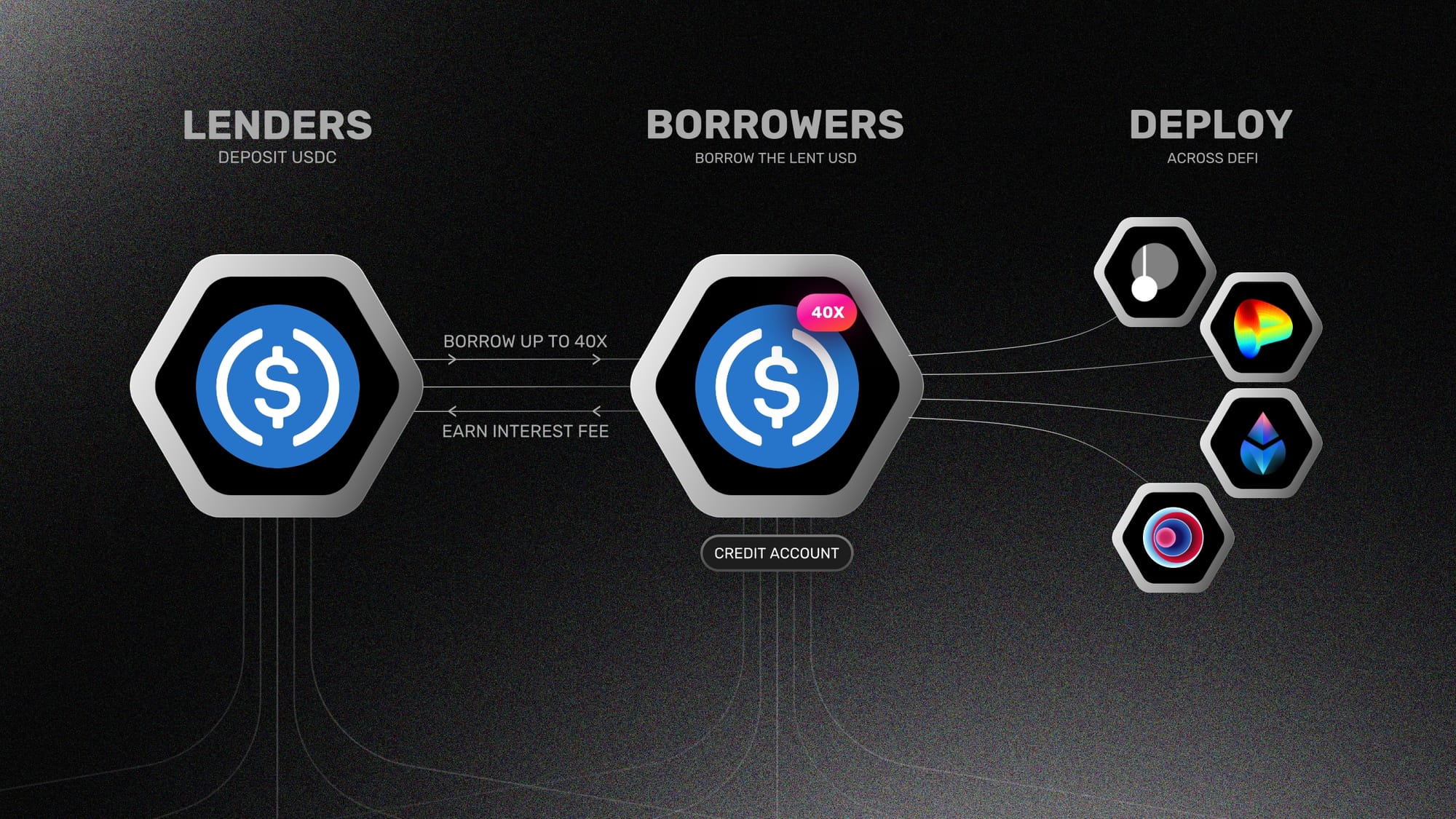

A Credit Account is similar to having a credit line for DeFi. It replaces the vending-machine like mechanism with a smart account-based system. Instead of depositing into a pool and borrowing from another, users can borrow up to 40X the collateral they deposit in their credit accounts and utilise it directly on external protocols.

This shift unlocks several structural advantages:

1. Contract-Level Execution

Credit accounts do not just hold assets; they execute actions on other protocols. They can call Pendle’s redemption function at maturity, Lido’s withdrawal flow, or Mellow’s mint/redeem logic. This preserves native behaviour and eliminates the need for DEX-based approximations and enable users to utilise protocols with the same efficiency they would otherwise.

2. Credit for non-tokenised assets

Because the system tracks the protocol-level position inside the credit account, it can recognise value that is not tokenised, such as Convex exposures, and extend credit against them.

3. Elimination of DEXes unlocks unmatchable UX

Settlement occurs through contracts, not through AMMs. This improves predictability, eliminates slippage, and preserves protocol-specific economic guarantees.

It also eliminates the need for DEX liquidity and saves issuers millions in annual costs, achieving the economic efficiency most institutions require and composability can deliver.

4. Structural Alignment With Institutional Workflows

Institutions operate through isolated accounts, mandates that have redemption periods, and controlled execution paths not pooled liquidity abstractions. Further, for assets not meant to be traded but just generate yield, these insititutions are unlikely to pay for DEX liquidity if they can have 0-cost redemption or minting option through vaults, like Mellow.

Credit accounts mirror this structure more closely, making institutional-grade composability credible. This has been explained in depth below.

This architecture turns composability from basic token interaction into an operational reality.

Why RWAs Will Make Real Composability Non-Negotiable

The coming growth of tokenised real-world assets will stress DeFi systems in ways that synthetic token listings cannot accommodate.

RWAs often have:

- issuer-controlled redemption windows

- fixed maturity schedules

- settlement processes involving custodians or registrars

- limited or no DEX liquidity

- legal and operational constraints on transferability as well as requirement for gated markets.

A pool-based architecture is structurally incapable of handling these features. It can only treat the asset as static collateral and rely on AMMs for liquidation, a model incompatible with assets that settle on issuer-defined rules.

By contrast, a credit-line architecture is naturally aligned with RWA mechanics:

- credit accounts can track redemption schedules

- adapters can encode issuer-settlement logic

- liquidation can occur through redemption rather than forced sale

- valuation can incorporate time-to-maturity and issuer conditions

- non-tokenised claims can still be recognised as economic collateral

RWAs will demand protocol-level integration, not token-level abstraction. They will require infrastructure that respects how assets settle, not how they trade.

This is precisely the environment where real composability, the kind enabled by credit-line systems, becomes indispensable.

This podcast by DeFi Dad provides a deep overview of how RWAs differ from the assets we have traditionally seen onchain.

🎙️ New @edge_pod

— DeFi Dad ⟠ defidad.eth (@DeFi_Dad) November 19, 2025

💸 The Next Generation of Tokenized RWA Yields in DeFi

0:00 - Intro

6:07 - Sonya’s background at Steakhouse

10:26 - Romeo’s background at Abraxas

17:33 - Appetite for institutional capital onchain

20:02 - State of looping in DeFi

25:37 - The mission behind 3F… pic.twitter.com/ueIdbdEINR

Where the future belongs

DeFi has spent years celebrating composability, yet most implementations reduce it to the simplest form of integration: listing a token. The consequence is an ecosystem that appears connected but loses the very efficiencies that make protocols valuable.

True composability requires more. It requires infrastructure capable of understanding and executing the full lifecycle of another protocol’s assets, rules, and settlement logic. It requires moving beyond vending-machine-style lending and toward architectures that treat protocols as interoperable systems, not as token containers.

As DeFi matures, and especially as RWAs move onchain, this deeper form of composability will determine which infrastructures scale and which remain limited to surface-level integrations.

The future belongs to systems that integrate protocols, not just the tokens they list.

If you are an institution or curator looking to expand your operations onchain, Gearbox can offer you the credit infrastructure you require. Contact us on Telegram or Discord, and get in touch. Let’s build the onchain economy together!

- Website: https://gearbox.fi/

- Main App: https://app.gearbox.fi/

- Telegram: https://t.me/GearboxProtocol

- Discord: https://discord.gg/gearbox

- Twitter: https://twitter.com/GearboxProtocol

- User Docs: https://docs.gearbox.finance/

- Developer Docs: https://dev.gearbox.fi/

- Github: https://github.com/Gearbox-protocol

- Snapshot page: https://snapshot.org/#/gearbox.eth

- Notion DAO monthly reports: