The End of Looping on Gearbox

Over the last few years, Gearbox became synonymous with looping. But we must admit: looping was never how leverage was supposed to work in DeFi. It was a workaround.

A clever hack that relied on DEX liquidity and flashloans to bypass the hard execution composability required. For five years, this recursive borrow–swap–deposit loop powered yields, strategies, and entire protocols.

But the mechanism that defined DeFi’s first era is fundamentally incompatible with the assets now coming onchain. As RWA issuers replace tokens, redemption replaces swaps, and compliance replaces permissionlessness, looping breaks. It is the end of an era, and Gearbox is now eliminating looping, exactly as we was always meant to.

This article examines the structural shifts reshaping onchain lending, how collateral is evolving from onchain derivatives to issuer-governed tokenized assets, why looping cannot adapt to this transition, and how composable credit evolves for RWAs. It covers:

1. Changing Lending Landscape

2. Stuck in Loops: Why looping is incompatible with RWAs

2. Eliminating Looping: RWA native Credit Lines

3. Midas Touch: The 1st issuer-credit instance

Read below to learn more!

I. Changing Lending Landscape

A defining theme of the current cycle has been the rapid acceleration of long-term structural shifts. Over the past year, regulatory clarity has increased, banks have revised their stances, institutions have rewritten their investment theses, and even traditional players like NASDAQ are rethinking their technology stacks.Shifts of this magnitude require more than incremental adjustments. They require lending infrastructure itself to evolve.

I. a) The Institutional Acceleration

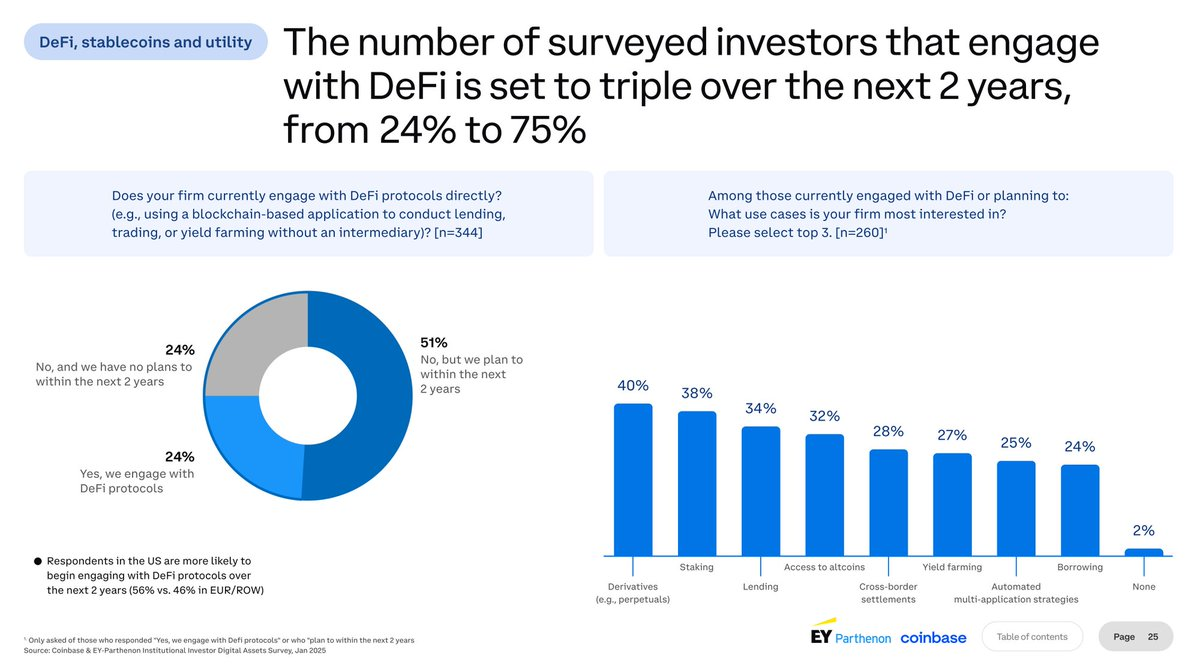

Institutions in DeFi aren't just allocating funds anymore, they are now active participants: as issuers, operators and policy makers. With and through the likes of @SuperstateInc, @Securitize, @MidasRWA and more, institutions are now working to bring TradFi structures onchain. The current participation, though, is just the beginning. A recent report by EY and Coinbase surveying 300+ institutions suggests

• Number of key institutions onchain will more than 3X over the next 2 years

• 4 of the top 8 use cases relate to lending, borrowing, yield-farming and composable strategies.

With lowering retail participation, institutions are key for DeFi protocols to grow over the coming years.

I. b) StreamFi and the end of low quality collaterals

DeFi’s history is marked by repeated collateral failures. From algorithmic stablecoins to opaque yield-bearing instruments, black-box structures have repeatedly collapsed under stress.

Recent events such as the StreamFi implosion, which left over $200 million in bad debt across lending protocols, further reduced tolerance for poorly defined collateral. These events were not isolated. UST, deUSD, and other failures have collectively driven appetite for unregulated, unverifiable collateral to historic lows.

— 0xmikko.eth (@0xmikko_eth) November 4, 2025

At the same time, institutional issuance is introducing a fundamentally different category of collateral. Tokenized equities, real estate, and private credit are not risk-free, but they offer defined redemption processes, legal claims, and issuer accountability. For the first time, DeFi is seeing collateral with properties comparable to traditional finance.

I. c) From "Assets" to "Issuers"

Traditional DeFi collateral is atomic. Tokens are freely transferable, continuously tradable on DEXes, and liquidated through open markets. Any constraints around minting or redemption are abstracted away by liquid wrappers.RWAs break this model entirely. They are issuer-led, regulation-governed instruments.Each RWA enforces a distinct set of rules around transferability, redemption mechanics, settlement timelines, and access controls. These mandates are enforced at the contract level by the issuer and must be respected by every holder, including lending protocols.Lending is no longer about just assets. It is also about issuers.

15. RWA looping will become a big trend, but it won’t look like atomic asset looping.

— Mippo 🟪 (@MikeIppolito_) January 1, 2026

Clever protocols will make use of offchain lenders and PBs who act as a bridge.

This will become a lucrative business line for PBs like Galaxy.

@mikeippolito_ highlights this mechanism. By eliminating looping, though, Gearbox can execute the entire process onchain, explained in section 2 and 3.

I. d) Compliance comes First

As institutions increasingly explore DeFi, assets issued and capital allocated by them increasingly looks for compliant markets. Regulatory clarity and institutional mandates now demand environments where compliance, transparency, and access controls coexist with decentralization. This is evident with the KYC requirement for projects like USDtb by Ethena, Tether Gold, Superstate, Centrifuge and other assets that have added $10B+ in TVL over the last year.For protocols, this means evolving beyond purely permissionless architectures to include gated markets, isolated pools or permissioned layers that allow KYC’d institutions to lend, borrow, and deploy capital within defined regulatory frameworks.

Together, these trends point towards a future with better quality collaterals issued by institutions that can be held accountable. While the traditional regulations and institutions ready themselves for DeFi, DeFi, too, needs evolve to with the evolving collateral standards. But we are still "Stuck in Loops."

II. Stuck in "Loops"

As DeFi transitions from onchain derivatives to issuer-governed RWAs, its most widely used leverage mechanism breaks.

How Looping works

In traditional pool-based lending, users deposit assets into shared liquidity pools and borrow from another pool. To achieve leverage, borrowed funds are swapped on DEXes into more of the collateral asset, redeposited, and borrowed against again. This loop is repeated multiple times.Flashloans compress this process into a single transaction by allowing users to borrow the full leveraged amount upfront, execute the loop, and repay the loan within one block.The model assumes:

- Continuous DEX liquidity

- Instant settlement

- Free transferability

- Market-based price discovery

RWAs violate all four.

Why looping breaks with RWAs

To understand why the mechanism of looping doesn't work with RWAs, lets look at why it fails with one of the largest RWA assets onchain, Superstate's USCC.

II. a) No DEX Liquidity

Superstate’s model for USCC is a tokenized share of a managed fund with subscriptions and redemptions done through the issuer, typically via USDC through Superstate infrastructure, rather than freely tradable liquidity pool tokens.Without DEX liquidity, the swap leg of the loop does not exist. Borrowed capital cannot be exchanged for the collateral asset through open markets.

II. b) No Flashloans

USCC enforces a 2+1 day redemption period but flashloans must be repaid within the same block.This means a user needs to pay back the loan before the asset is redeemed, rendering flashloans incompatible with RWAs.

II. c) Inefficient Unwinding

Even without flashloans, manual looping creates untenable exit risk.A user who loops an asset ten times must effectively wait through the redemption window ten times to unwind. A three-day redemption becomes a month. A 30-day redemption becomes a year.This increases the risks lenders are exposed to and not just the issues borrowers face.

II d.) Restricted Transferability

Many RWAs enforce whitelists, KYC, transfer limits, or jurisdictional rules at the contract level. Looping requires assets to move freely between protocols. If transfers are restricted, redepositing or liquidating becomes impossible.With more complex RWAs like equities, looping falls completely flat. And that's why, after 4 years, Gearbox is eliminating looping.

III. Eliminating Looping: RWA Native Credit Lines

The issue with looping isn't flashloans or DEX liquidity, but the design of lending protocols that forces them to rely on external tools and middlemen. Most lending protocols are composable with token standards (ERC-20 etc) and not other protocols. They need DEXes for swaps, flashloans for leverage and tools like Contango for execution. Their architecture cannot enforce issuer mandates, redeem assets, or scale to RWAs. That's why, Gearbox is eliminating looping. And replacing it with RWA native Credit Lines.

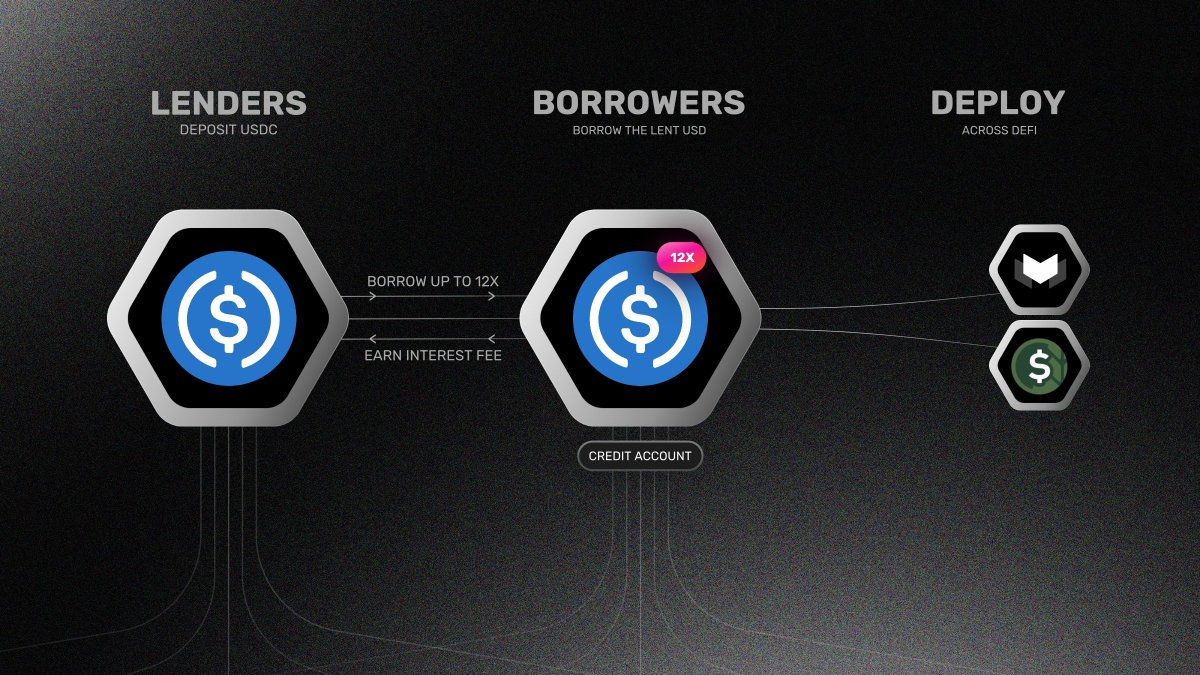

Meet RWA Credit Lines

The ideal leverage mechanism for RWAs should deliver credit natively at an issuer's contracts while complying with any risk and compliance mandates, akin to a real world credit line. And that's what Gearbox delivers.At the heart of this is our pool-to-account model. Borrowers on Gearbox open Credit Accounts that aren't just composable with tokens but also protocols. These CAs act as a smart wallet that can plug in at the contract level of vaults, RWAs, protocols and any smart contract.

How Do They Work

Credit Accounts are isolated smart contracts that function as programmable credit lines. Borrowers deposit collateral into a CA, borrow from the lending pool, and interact directly with issuer contracts to mint or redeem RWAs.

CAs can be programmed to follow the exact mandates, redemption periods and minting constraints an issuer requires while delivering leverage directly at the contract without the need of DEXes, flashloans or any external tools.

This also unlocks unique lending features and benefits.

Leverage Without DEX liquidity: 0 Slippage, 0 liquidity costs, 0 friction

Traditional lending protocols don't just rely on DEXes for liquidity, they model their risk parameters as per DEXes. Since DEXes have a fraction of liquidity that contracts do and are prone to sizeable price impacts, they limit the capabilities of onchain lending. By lending directly at the contract level, Gearbox

• Reduces slippage and DEX fee to 0, saving months of yield

• Unlocks highest LTVs in DeFi, borrow more for every dollar

• Unlocks $B+ Scale, scale multiple times more than other protocols

• Lower Liquidation points, safer positions

• No DEX liquidity required, saving millions in costs for issuers

• Unwind positions in fraction of days, save costs with higher efficiency

Gearbox can thus adapt to any asset design and let institutions scale with the highest level of efficiency.

Battle-Tested Architecture

What further sets Gearbox's Credit Accounts apart is their secure, battle-tested nature. CAs have been live since 2021 without ever facing a security issue or exploit. During this period:

• They have gone through 10+ rigorous audits

• Solidified via whitehack bounties

• Fortified through $3M+ in security investments

• Survived multiple black swans and risk events

Thus offering infrastructure that isn't just delivering the most efficient lending mechanism onchain but also the robust security RWAs need.

IV. The first Credit Line is now Live!

The mechanism discussed above isn't theory or description of an ideal state DeFi lending must achieve but a product Gearbox has already delivered. The first Credit Line for RWAs went live on Monad for Midas. Users can access up to $1 million in credit while minting mEDGE through issuer contracts by Edge Capital.

Borrowers burn billions on slippage. Issuers lose millions bootstrapping liquidity. DeFi loses efficiency. No more.

— Gearbox Protocol (@GearboxProtocol) December 24, 2025

The first real credit-line for RWAs is now live. Mint mEdge via @MidasRWA's contracts with up to $1M in credit.

0 slippage, 0 DEX reliance, 7X faster unwinding↓ pic.twitter.com/HEHrX6mRJc

With a two-day redemption period, Gearbox enables users to unwind their entire leveraged position in a single step. Equivalent loop-based positions would require weeks to exit.Experience the evolution of DeFi lending on Monad: app.gearbox.fi

Ending Note

Looping was a bandaid to a problem DeFi needed a surgery for. It emerged in a world where leverage had to be manufactured from pools, swaps, and flashloans because native credit did not exist. That world is ending. As issuers, compliance, and real-world assets reshape onchain collateral, leverage can no longer rely on recursive market hacks. It must be issued directly, enforced at the protocol level, and aligned with how assets actually function. The transition away from looping is not a retreat from DeFi’s original vision, it is its maturation. The next era of onchain lending will not be built on loops and middlemen.

It will be built on credit.

It will be built on composability.

It will be built on Gearbox.

If you are an institution or curator looking to expand your operations onchain, Gearbox can offer you the RWA credit infrastructure you require. Contact us on Telegram or Discord, and get in touch. Let’s build the onchain economy together!

- Website: https://gearbox.fi/

- Main App: https://app.gearbox.fi/

- Telegram: https://t.me/GearboxProtocol

- Discord: https://discord.gg/gearbox

- Twitter: https://twitter.com/GearboxProtocol

- User Docs: https://docs.gearbox.finance/

- Developer Docs: https://dev.gearbox.fi/

- Github: https://github.com/Gearbox-protocol

- Snapshot page: https://snapshot.org/#/gearbox.eth